AI Surge Bolsters Electronics Industry from Geopolitical Headwinds

Hong Kong Electronics Fair 2026 (Spring Edition) Survey Results

Highlight

- Short- and medium-term growth sentiment rose to 48% and 59%, respectively, both higher than the Autumn 2025 survey, signalling strengthening momentum in the global electronics sector despite geopolitical headwinds.

- Artificial Intelligence is viewed as the most influential technology, ranking well above other innovations. Strong interests in smart home and robotics reflect the rising demand for intelligent, automated solutions.

Growth momentum is expected to be maintained in the global electronics sector throughout 2026, according to the majority of industry players surveyed during the most recent HKTDC Hong Kong Electronics Fair (Spring 2026)(EFSE). With 648 industry players participating in the survey, 48% anticipated sales growth in the short term (the next six‑to‑12 months), while 59% were optimistic about prospects over the medium term (the next 12‑to‑24 months). Reassuringly, positive short‑term and medium‑term sales sentiment were both up compared to the findings of the corresponding survey conducted during the event’s Autumn 2025 iteration.

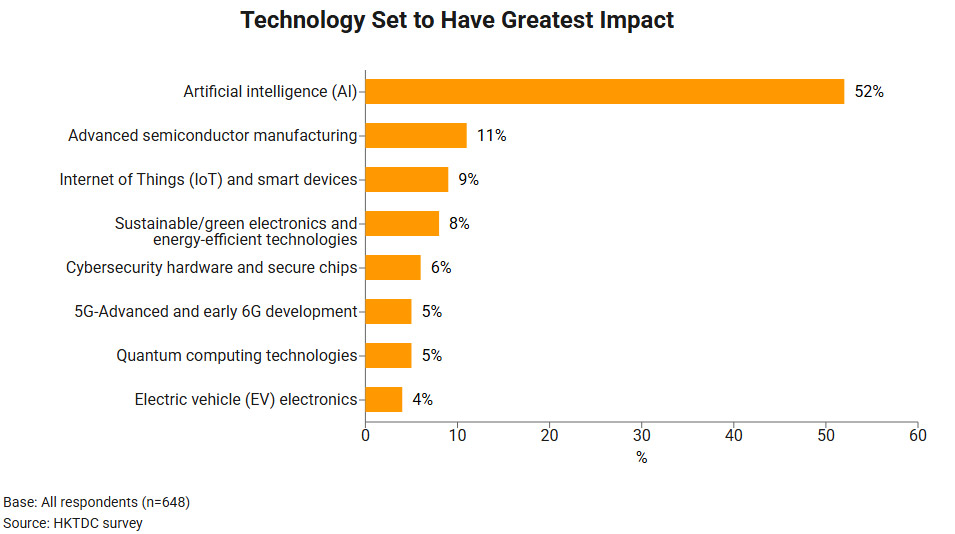

In terms of the technology set to shape the industry over the next two years, Artificial intelligence (AI) was widely seen as likely to have the most impact, a sentiment shared by more than half of all survey participants – an outcome that ranked it significantly higher than many other trending advances, notably semiconductor manufacturing. In terms of the segments seen as having the greatest growth potential, smart home/living products received the most backing (29%), followed by robotics (21%). This can be seen as reflecting the growing demand for automation and AI‑enabled applications, while also indicating a broader technological shift toward intelligent, connected ecosystems.

It was also notable that the industry’s upbeat sentiment persisted despite the many current geopolitical uncertainties, including the Middle East conflict, which was ongoing throughout the survey period (13‑16 April 2026).

Promising sales prospects

Overall, the survey showed that many electronics traders were broadly optimistic with regard to their future market prospects. Indeed, most respondents expected their overall sales to either rise or, at least, remain stable over both the short term (six‑to‑12 months) and the medium term (12‑24 months). More specifically, 48% of respondents anticipated sales growth in the short term (with 45% expecting sales to remain stable), while 59% foresaw growth in the medium term (with a further 37% expecting a stable sales performance). It was also notable that the sales outlook has rallied somewhat compared with the sentiment recorded during the Autumn 2025 edition of the Electronics Fair, with the proportion of respondents optimistic about future growth rising from 32% to 48% over the short term, and from 51% to 59% over the medium term.

New technology

It was also notable that artificial intelligence (AI) remained very much the priority for the majority of survey participants. As testimony to this, more than half of the surveyed companies saw AI as the technology likely to have the most impact over the next two years – an outcome that placed it significantly ahead of other emerging trends, including advanced semiconductor manufacturing (11%) and IoT and smart devices (9%).

Most popular product categories

In terms of product categories tipped to do well, smart home/living products and solutions sectors (29%) and robotics products (21%) were seen as having the highest growth potential. Robotics was also highlighted as a segment with particularly strong momentum, while lagging only slightly behind (as cited by 18% of respondents) were electronic/electrical accessories. Overall, the survey findings reflected rising demand for automation and AI‑enabled applications, while also indicating a broader shift towards intelligent, connected ecosystems.

Mainland and ASEAN in the spotlight

While the views of individual regions tended to vary, overall, respondents were particularly optimistic with regard to their prospects in Chinese Mainland, several Asian markets, and Northern & Western Europe. On a five‑point scale, with ‘1’ denoting ‘very unpromising’ and ‘5’ equating to ‘very promising’, Mainland was seen as having the greatest potential (3.83), followed by the ASEAN bloc (3.69) and the Northern & Western Europe (3.65).

Challenges on the horizon

Assessing the impact of the Middle East conflict, 27% of respondents indicated they had experienced either ‘limited’ (17%) or ‘no significant impact’ at present (10%), with 43% describing the impact as ‘moderate’ and 10% as ‘significant’. A further 20% maintained they had been ‘indirectly impacted’ (e.g., affected by rising fuel prices or declining market confidence). In terms of moves to mitigate any negative consequences, respondents indicated they had explored a range of strategic options, including evaluating contingency plans (33%) and assessing various risk diversification measures (24%).

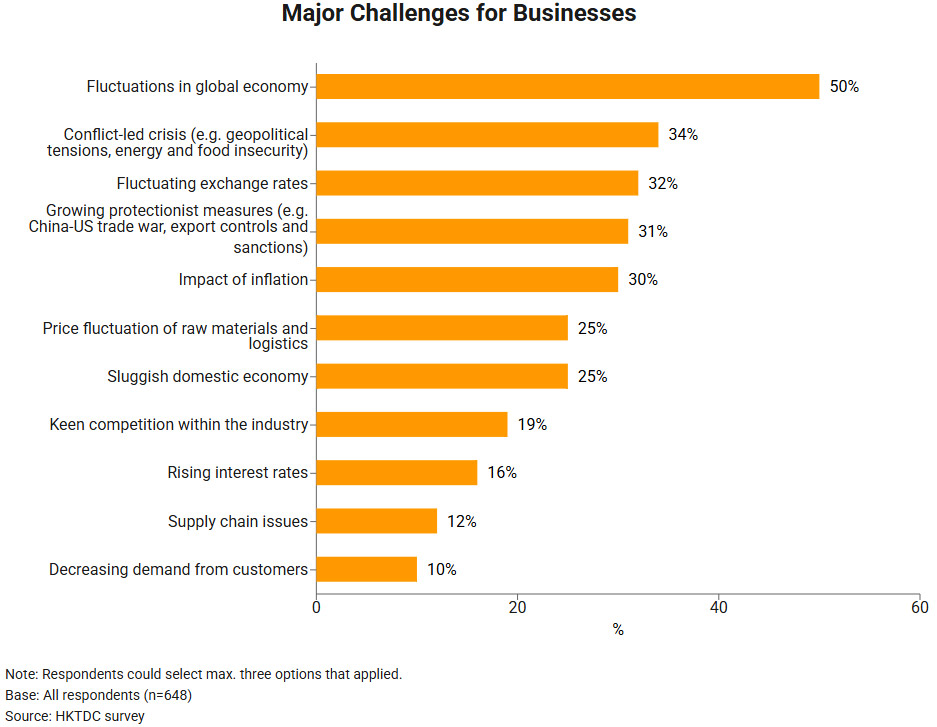

In addition to broader macroeconomic uncertainties – particularly fluctuations in the global economy (50%) – many survey respondents expressed concerns over the level of geopolitical risk. This concern was primarily focused on such conflict‑driven crises as geopolitical tensions and energy insecurity (34%), as well as exchange rate volatility (32%) and rising protectionism (31%).

Profile of respondents

- 258 exhibitors – 54% from the Chinese Mainland, 33% based in Hong Kong, and 13% from the rest of the world.

- 390 buyers – 38% based in Hong Kong, 33% from the Chinese Mainland, 29% from the rest of the world.

The 2026 Hong Kong Electronics Fair (Spring Edition) took place from 13-16 April at the Hong Kong Convention and Exhibition Centre.

Original article published in https://research.hktdc.com